Choosing the Right Digital PR Firm for Your Business

198 ViewsFinding the right partner to support your online growth can significantly influence how your brand is seen, discovered, and trusted. Digital PR firms play a crucial role in building

Read More

Why Loan Prepayment Conditions Matter More in Long-Tenure Vehicle Loans

144 ViewsBuying a car often feels like a balancing act between the monthly budget and the total cost of ownership. As vehicle prices rise, many buyers are turning to longer

Read More

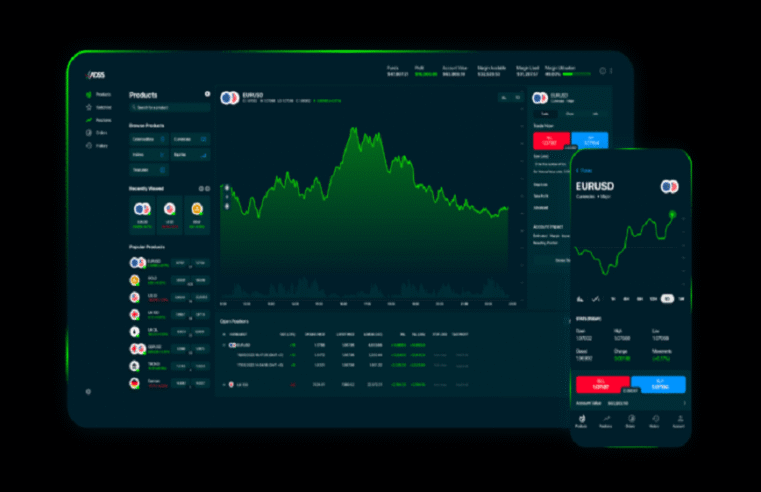

How Investors Track Market Movements Through CFD Positions

143 ViewsFinancial markets move rapidly, influenced by economic reports, global events, and shifts in investor sentiment. For investors, keeping track of these movements is essential for making informed decisions and

Read More

Utah Asphalt Contractor Services for Durable and Long-Lasting Pavements

153 ViewsCommercial properties depend heavily on well-maintained pavement to ensure safety, efficiency, and a professional appearance. Whether it is a retail center, office complex, warehouse facility, or industrial site, the

Read More

The Hidden Advantages of Choosing a Member-Owned Financial Institution

142 ViewsMost people think all banks work the same way. They don’t. Member-owned financial institutions flip the entire banking model upside down. Instead of customers feeding profits to shareholders, members

Read More

What Happens to Spent Catalyst After a Change-Out? Handling, Storage, and Recycling Best Practices

316 ViewsCatalyst change-outs happen all the time in industrial operations. They’re particularly common in refining, chemical processing, and environmental systems. Most planning centers on one thing: get the old catalyst

Read More

NRE vs. NRO vs. SNRR accounts: What suits your global portfolio best?

231 ViewsFor Non-Resident Indians (NRIs), managing money across countries requires careful planning and the right banking structure. Whether your earnings originate abroad, within India, or through targeted investments, three key

Read More

Steps to Building a Positive and Productive Organization

157 ViewsEmployee disengagement can quietly undermine business performance. When dissatisfaction grows due to a strained workplace culture, limited compensation or benefits, heavy workloads, or chronic stress that leads to burnout,

Read More

Nifty 50- A Mirror to India’s Financial and Economic Growth

224 ViewsThere have been big changes in India’s finances over the last few decades, and the Nifty 50 measure is a key sign of these changes. The Nifty 50 is

Read More

4 Types of Underwriting Criteria in the Hard Money Industry

233 ViewsHave you ever heard claims that hard money lending is ‘last resort’ lending for desperate borrowers who cannot get conventional bank loans? If so, forget them. Hard money lending

Read More